My thoughts on TCS

Tata Consultancy Service, founded 52 years ago, is currently India's second-largest publicly traded company. It has a market cap of Rs. 640,000 Cr or about $80 billion.

India's current GDP is around $2.7 Trillion. That makes TCS about 3% of Indian GDP. That is huge. It currently employees more than 400,000 people across 46 countries.

Just because of its size, TCS has to operate across various verticals. It has clients across:

- Banking

- Retail and CPG

- Communication and Media

- Manufacturing

- Life Sciences and Healthcare

- Technology & Services

Currently, it's fastest-growing vertical is Life Sciences and Healthcare. It is growing at ~17% annually, followed by communication and media at ~10% growth.

Speaking at growth, let's look at some numbers.

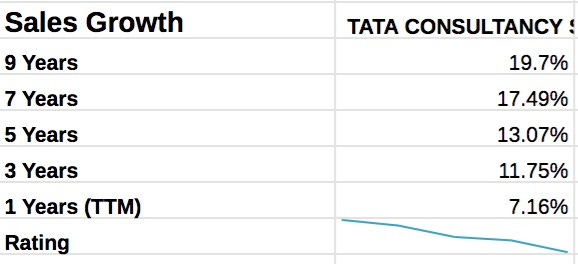

Starting with the sales growth rate, TCS has grown at about 20% CAGR for the past 10 years. But, growth has been slowing. It only grew at about 12% CAGR for the past 3 years.

That is a solid top line. Now let's look at the bottom line.

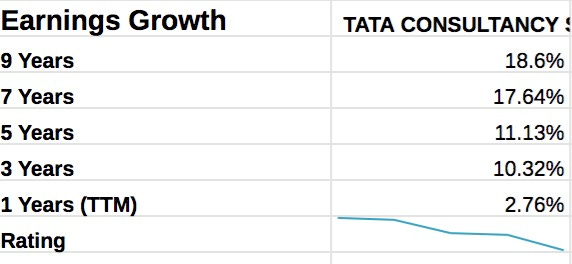

TCS has an 18.6% 10-year CAGR earnings growth. That growth has dropped to 10% for the last 3-years.

Great numbers for both top and bottom line, and both tell the same story, that of transitioning from a growth to a mature company.

Revenue Mix:

Where does TCS get its revenue?

More than 50% comes from North America, 30% from Europe and only 5% from India!

TCS is a pseudo-Indian company.

Management:

For management, I like to look at the return on equity(ROE) and return on invested capital(ROIC).

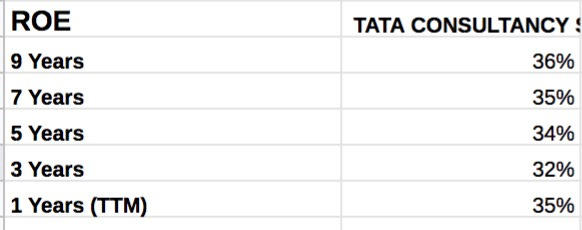

The average ROE over the past 10 years for TCS is 36%, and ROIC is 43%. Only 16 other publicly traded companies in India can claim that. TCS has been able to keep high ROE and ROIC for the past 10 years; It indeed has one of the best management.

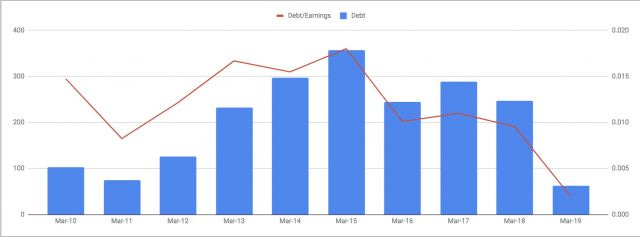

Another way to judge management is to look at how they are managing debt. Although the software industry is not a capital intensive business, it's not a bad idea to see how management handles financing.

TCS currently has about Rs. 8,000 Cr of debt on its balance sheet; it is more than manageable. With earnings of Rs. 32,000 Cr, they can pay down all the debt with a quarter's worth of profit (not saying that they should). The debt compared with earnings have been very manageable since 2010. Signs of great capital allocation!

Ok, so TCS is a business leader with high-quality products, excellent management. Now the big question, should you buy it?

One of the most popular ways to measure if a company is undervalued or overvalued is to look at its Price to Earnings ratio or PE ratio.

TCS is trading around PE of 20. In the past 10 years, the minimum PE was 18, and the maximum PE was 25. It is definitely trading towards the lower end of its historic range.

I think TCS has a great moat in a relatively fast-growing industry. It is a market leader with an excellent management track record. The likelihood of TCS growing at 20% in the next decade as it did in the past decade is pretty low. If it did grow at 20%, it would account for more than 23% of India's GDP (as mentioned earlier, it's at 3% right now).

Having said that, because it gets its revenue from so many different regions, adding that in your portfolio, instantly diversifies geographical risk + a stable dividend growth, buybacks, and strong industry tailwinds.

You can do a lot worse than TCS.