My thoughts on Maruti

Maruti Suzuki

Founded in 1982 is India’s 14th largest company. It is currently worth some 160,000 Cr. Maruti dominates India’s four-wheeler market share with more than 50% in most passenger vehicles categories.

The company recorded its highest-ever sale in FY19 of about 1,862,449 units.

The Macro:

Let’s look at the whole pie. India’s GDP is currently at Rs. 210 Trillion. The auto industry contributes about 7% to India’s GDP, which makes the auto industry market in India of about Rs. 14 Trillion.

Of that, only ~18% is four-wheelers. The total market for four-wheelers in India comes to Rs. ~2.5 Trillion. Almost there!

Maruti commands about 50% of the four-wheeler market, so Maruti’s potential market size is ~1.25 Trillion or Rs. 125,000 Cr.

Maruti’s total revenue in the year 2019 was Rs. 86,000 Cr. There is enough pie left for Maruti to capture.

India’s auto industry is expected to grow at the same rate as the GDP, about 5-7%. Market leaders generally grow double the rate of the industry.

That would mean Maruti’s sales should grow at about 14% every year for the next 10 years.

Now that we have an estimate of Maruti’s future revenue growth rate, let’s look at the company’s historical performance.

Moat:

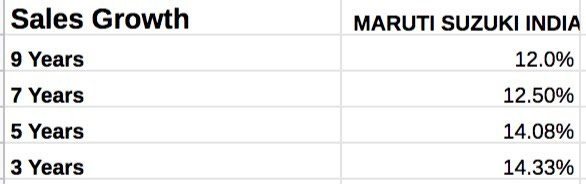

Starting from the top. Maruti has a 10-year CAGR of 12% and has been able to maintain growth between 12-14%.

The same for the bottom line. Healthy profit growth of about 12% CAGR for the past 10-years.

While moats are usually qualitative, one way to quantify is to look at the pre-tax profit margin. The industry profit margin is ~8%, Maruti has been able to maintain it well above the average at ~13%.

Management:

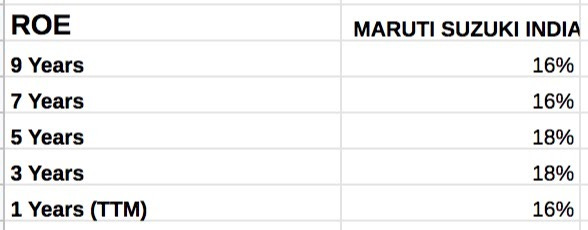

For management, I like to look at the return on equity(ROE) and return on invested capital(ROIC).

Average ROE and ROIC for Indian companies are 7.8% and 12%, respectively.

Maruti scores above average for both.

Debt:

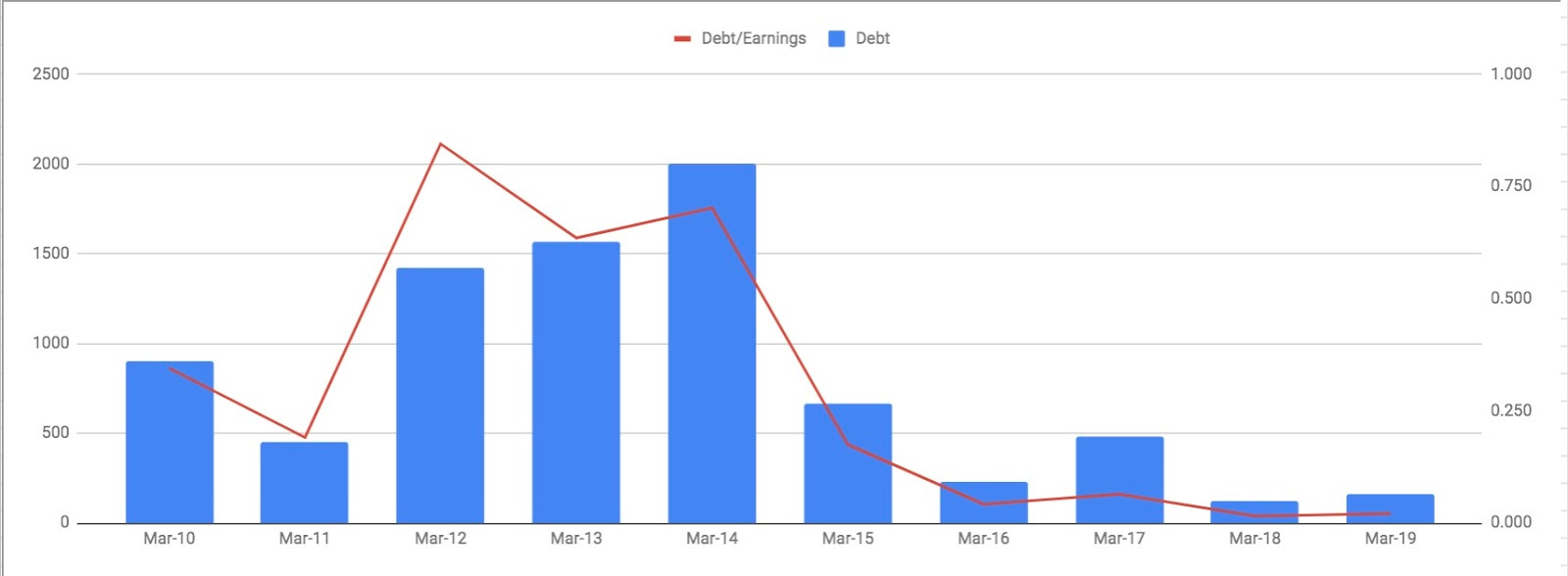

Maruti has a debt of 400 Cr. and has an annual profit of 7600 Cr. That is about ~150 Cr profit every week. It can pay down all its debt in a month!

We can see the same pattern looking at its history-

Red Flags:

Cars are discretionary for the most Indian consumer, and in these COVID-19 recession times auto sales will take a beating

The current production capacity of Maruti is about 200,000 units and sold about 180,000 units last year. It is reaching its capacity limit, and they will have to increase capacity very soon

The export of cars was a faster-growing segment for the company than domestic sales. Export only grew 3% last year, and the demand is still very weak from the overseas market

Need to invest more in electric automobile infrastructure, including EV and recharging stations

Bottom Line:

Maruti is an Indian gem. It employs millions of people. It was the first Indian company to export a car to Japan!

It has been growing 2x Indian GDP, and there is a very high likelihood of that continuing in the next decade

Winners keep winning. Dominant player is difficult to topple, especially in a business with such a high barrier to entry

The product it sells do not require constant innovation

It has a strong moat with excellent management

I would buy this tremendous Indian company every time it drops 10%

Please let me know what you think! I would love to get some feedback. Just hit reply to this mail!