My thoughts on Eicher Motors

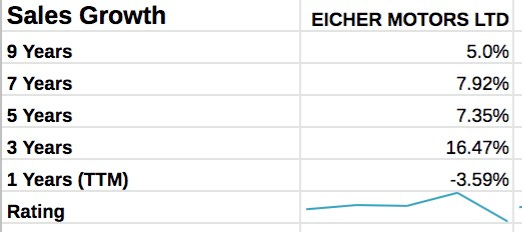

Eicher Motors has been around since the time of India's Independence, the company started as a tractor company but now is a market leader in two-wheelers. You might recognize their products by the name of Royal Enfield. Eicher Motors has fallen about 40% from its highs in recent weeks because of the pandemic! Has it fallen enough, is it time to buy? Before we answer that, let's look at what the company does. Eicher Motors has two types of products: two-wheelers and trucks and buses. Eicher has partner with Volvo to sell trucks and buses, but that remains a tiny portion of Eicher's revenue at the moment, only about 10%. The majority of the revenue comes from Royal Enfield bikes. Royal Enfield owns more than 90% market share in the mid-size motorcycle segment. The current average revenue per bike is about Rs.120,000, which is nearly a 20% increase in the past five years. They sold more than 800,000 motorcycles last year, which is also growing at a nice pace for the past few years. Let's dig deeper into the numbers, starting with the top line. Eicher was slow to grow, but in the past three years, its sales have been growing at more than 15% every year. 2019 saw some drop in the growth rate but nothing major.

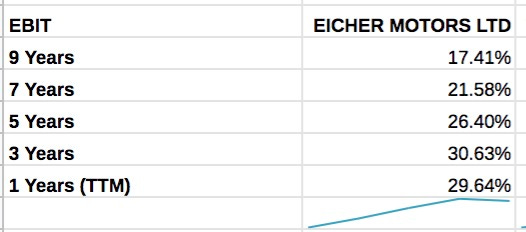

Now, for the bottom line, Eicher has been growing north of 30% CGAR for the past ten years, most of that growth coming in the middle of the decade.

Eicher Motors also have healthy margins and have been able to increase it too.

Management:

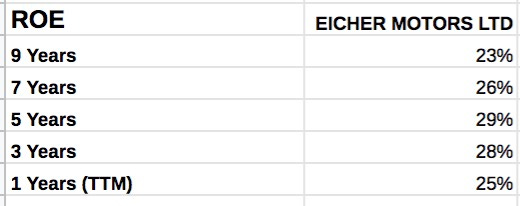

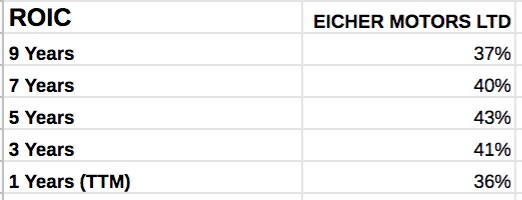

I like to look at Return on Equity and Return on Invested Capital to judge the capital allocation of the management. For Eicher Motors, the management has been phenomenal, ten-year average ROE of 20%+ and ten year average of ROIC of 30%+.

Another indicator to judge the management is to look at the company's debt. Debt for Eicher is well under control. They have a debt of about 164 Cr as of now on their balance sheet and quarterly net profit of 500 Cr. They can pay down all their with two months of profits.

So to summarise, Eicher Motors has been able to grow revenue, increase the number of units sold, increase margins, increase operating profit, and not increase debt. All this sounds great!

And then this happened:

Eicher sold 63,500 Royal Enfield bikes sold in January 2020 but only 91 in April 2020. 63,500 to 91 is a significant drop, and there are no signs of those numbers improving in the short term.

Bottom Line:

Two-wheeler is a growing market segment in India, and Royal Enfield is a market leader.

Royal Enfiled is a cash cow for Eicher Motors with margins more than 25%

Royal Enfield has a brand moat. People love the product and are loyal to it.

Being a premium product, it might take longer for the demand to recover.

There are multiple plants under construction to increase capacity.

There are growth opportunities in the exports for trucks and buses business.

Excellent management who have kept balance sheet strong.

There is a high likelihood that Eicher motors will weather this storm and come out of it stronger.