Did David Wallace overpay?

In the previous letter, Micheal Scott Paper Company(MSPC) was bought out by David Wallace's Dunder Mifflin (DM). But did David overpay for MSPC? Or did he make a great deal?

To find out, I'll try first to calculate a fair value for MSPC and then calculate how much it would cost DM to re-hire Micheal, Pam, and Ryan.

The fair value of MSPC:

Before we move on, we need to take a step back. A fundamental concept for valuing any asset is the Time value of money.

I'll let Fred Wilson take over to explain Time value of money:

Money today is generally worth more than money tomorrow.

Money in your pocket, cash in hand, is worth more than cash that you don't actually have in hand. If you think about it that simply, everyone can agree that they'd rather have the cash in hand than the promise of the same amount at some later day.

And interest rates are used to calculate exactly how much more the money is worth today than tomorrow. Let's say that you'd take $900 today instead of $1000 exactly a year from now. That means you'd accept a 11.1% "discount rate" on that transaction.

Interest rates and discount rates are generally the same thing.

So if the interest rate describes the time value of money, then the higher it is, the more valuable money is in your hands and the less valuable money is down the road.

Now that we have that let's move on to the Discounted Cash Flow(DCF) model.

There are few components to DCF valuation, an asset. And each part comes with its own set of assumptions.

Here are some of the elements of my valuation system:

Revenue

Profit margin

Earnings/Profits

Earnings Growth

Cost of capital/expected rate of return

Terminal cash flow

The complete system looks something like this:

The first thing we need to begin is MSCP's annual revenue.

We will have to estimate how much revenue Micheal Scott Paper Company stole from Dunder Mifflin.

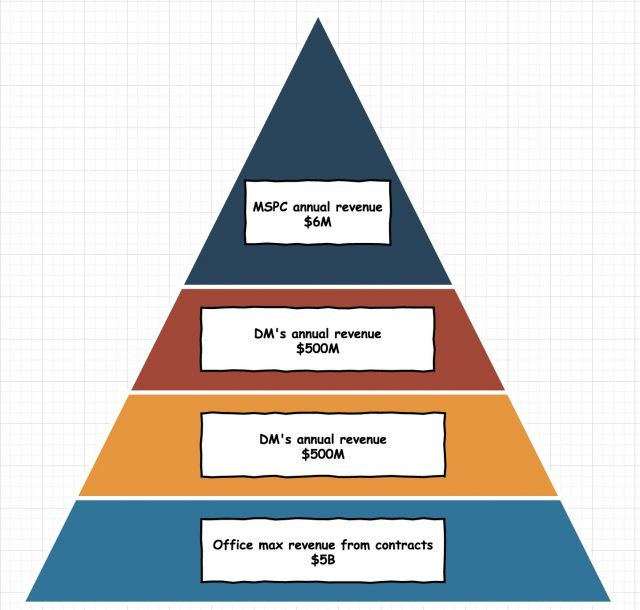

Since we can't find financial docs of MSPC or DM, we'll look at the next best thing, Office Max. I dug up Office Max's annual report from 2007.

Here are some of the missing pieces we need:

Office Max's yearly revenue in 2007 from the "OfficeMax, Contract" segment(most similar to DM's business model) was about $5 billion.

Since DM is a much smaller company and only operates on the east coast, we'll assume DM is about 10% the size of Office Max. That makes DM's annual revenue of ~$500 million.

Next, we need to know how much the Scranton branch's revenue was in 2007. We know that the Scranton branch is the most profitable branch in the company. The best salesman at the company also works for the Scraton branch!

DM had 7 branches operational at the time.

Let's apply the Pareto principle, meaning 20% of branches bring in 80% of the revenue or 2 branches bring in $400 million in revenue. Let's split that between Scranton and some other branch.

To summarize, the Scranton branch brought in about $200 million in sales for the year 2007.

Let's say Micheal was able to steal 3% of DM's revenue. That makes revenue of MSPC: ~$6 million.

We now have enough to begin our DCF model.

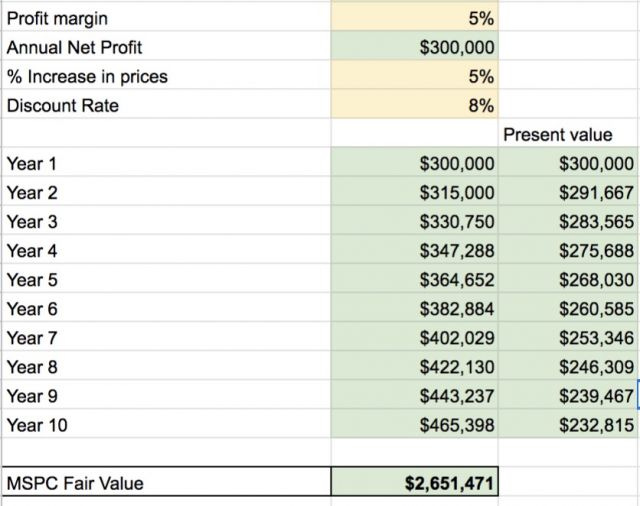

Next, we need to estimate the net profit margin of MSCP. Office Max and Staples had about 3-5% margins in 2007. Let's give the MSCP 5% profit margin.

That makes annual profit or earnings of MSCP of $300k.

We can pause here and do a back of the envelope calculation to estimate the value of MSCP. A general rule of thumb is that a publicly-traded company is worth about 20 times its profit or a 20 PE, whereas a private company is worth about 10 times its annual profit. Since MSCP will make an estimate of $300k in profit, that puts its value at $300k x 10 = $3 million.

Let's look at a more sophisticated model.

We will grow MSCP's profit by 5% every year for the next 10 years and then apply a "discount rate" or returns that we expect to make on an investment. US markets have returned about 8% returns over the long term; we can use that as our discount rate. We will ignore the terminal value for this model.

This model puts MSPC's value at $2.6 million.

Now that we know MSCP is worth between $3-$2.6 million, how much did David Wallace agreed to pay for it?

That is pretty easy to calculate.

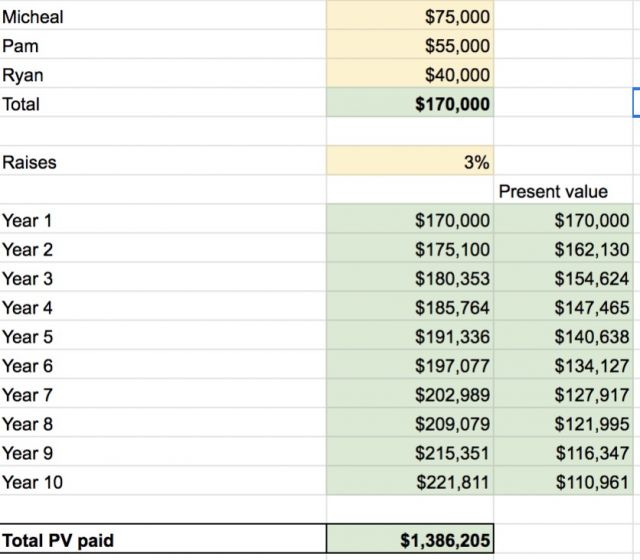

I'm assuming Micheal's salary is $75k, Pam's $55k, and Ryan's 44k, totaling DM's liabilities to $170k.

Let's say they get raises of about 3% each year for the next 10 years and then discount those salaries by the same discount rate to bring DM's liabilities to present value. That is a total payment of ~$1.4 million.

To summaries, Micheal Scott Paper Company's fair value is ~$2.6 million, and David Wallace will end up paying ~$1.4 million.

In other words, buying MSPC will most likely generate a value of ~2.6 million for DM, for which they are only paying ~$1.4 million. That is a total steal for David Wallace and Dunder Mifflin. Good job, David!

This, of course, is an oversimplification of how valuations are done but feel free to check out the complete model here. Make a copy and change the numbers that you disagree with. Yellow cells are inputs; green ones are automatically calculated. As you would see there are quite a bit of yellow/input cells and each yellow cell comes with assumptions attached to them. Any model is as good it's assumptions.

Valuation is more art than science. Also, none of this would have happened if David Wallace returned Micheal's calls.

Let me know what you think? What incorrect assumptions I made? What did I overlook?