I’ve been binging Patrick O' Shaughnessy’s “Invest like the best” podcast for the last few days. Highly recommend for anyone interested in investing in early-stage tech companies.

One of the guests, while explaining exploding compound growth, gives an example of Facebook. For a long time, people complained when Facebook was going to make money, but no one bothered to look at the large userbase it was amassing. Same thing with Google. These companies build large userbase and then found a way to monetize them.

Revenue for Facebook over the last 10 years-

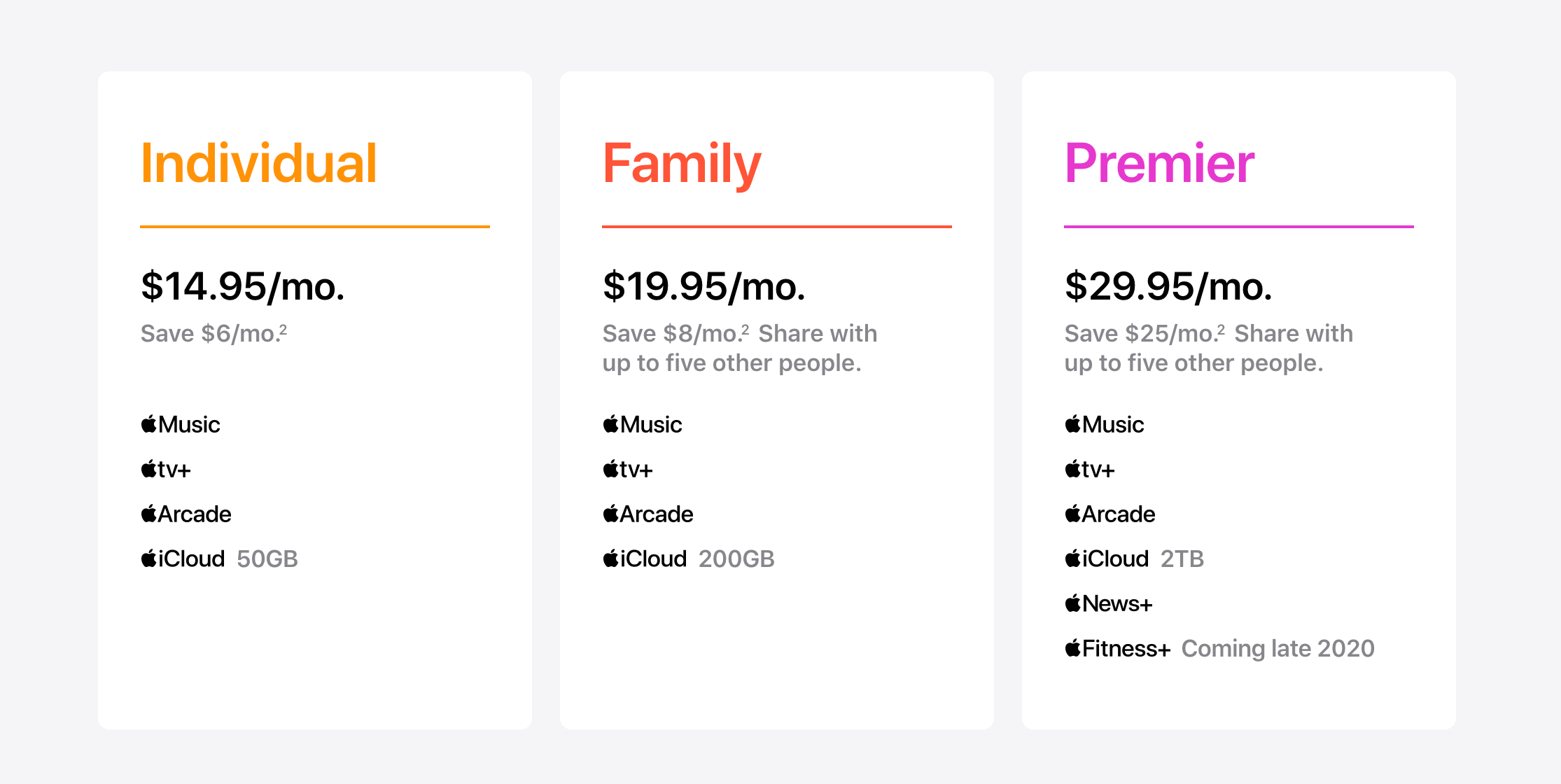

Apple had an event yesterday, and one of the most important announcements, I think, was Apple One!

Like Facebook and Google, Apple has amassed a huge userbase (one billion users), and its now time for them to monetize it via a rundle (recurring bundle of services).

Apple One combines Apple’s multiple services into one bundle. While I currently only pay for the iCloud service, I think there is potential for Apple to further strengthen its recurring revenue stream.

Two reasons why I think Apple One will be huge are-

Family Sharing: While the Apple ecosystem has an extremely high switching cost. That switching cost becomes exponentially higher if your whole family has an iPhone or iPad. Paying one price for multiple services that can be used by the whole family is convenient + sharing that iCloud space across members is also a great value-add.

Ability to keep adding new services: Using just an iPhone by itself is great, but it gets exponentially better when you have an Apple watch and an iPhone. When you add-in AirPods, the value of the whole network/ecosystem increases exponentially again. That is why Apple had such great success with its wearables. With Apple One, they can do the same thing on the software side. They can keep bundling new services into one, increasing the value for the consumer.

As an investor, there is nothing better than an asset that produces recurring revenue, which is a high margin, inflation resistant, and increases moat (Apple One increases the switching cost even higher).

With such a high loyal user base, if Apple can do what Facebook and Google have been able to do, I think Apple’s service revenue will be higher than revenue from iPhone/iPad/MacBook's sale very soon which will in-turn generate huge shareholder value.

PS-

If you’re interested in learning about moats and different moats, we did a deep-dive in the recent episode of Cold Brew Money. Check it out.

Interesting take.

Agreed on the super sticky moat from using the premium "apple ecosystem".

Would be even more intriguing if the Churn rate & absolute engagement #s, from the Apple ecosystem, in the past few years can be known... Unsure if apple actually discloses these though..

Very very interesting! I was thinking of the same thing yesterday